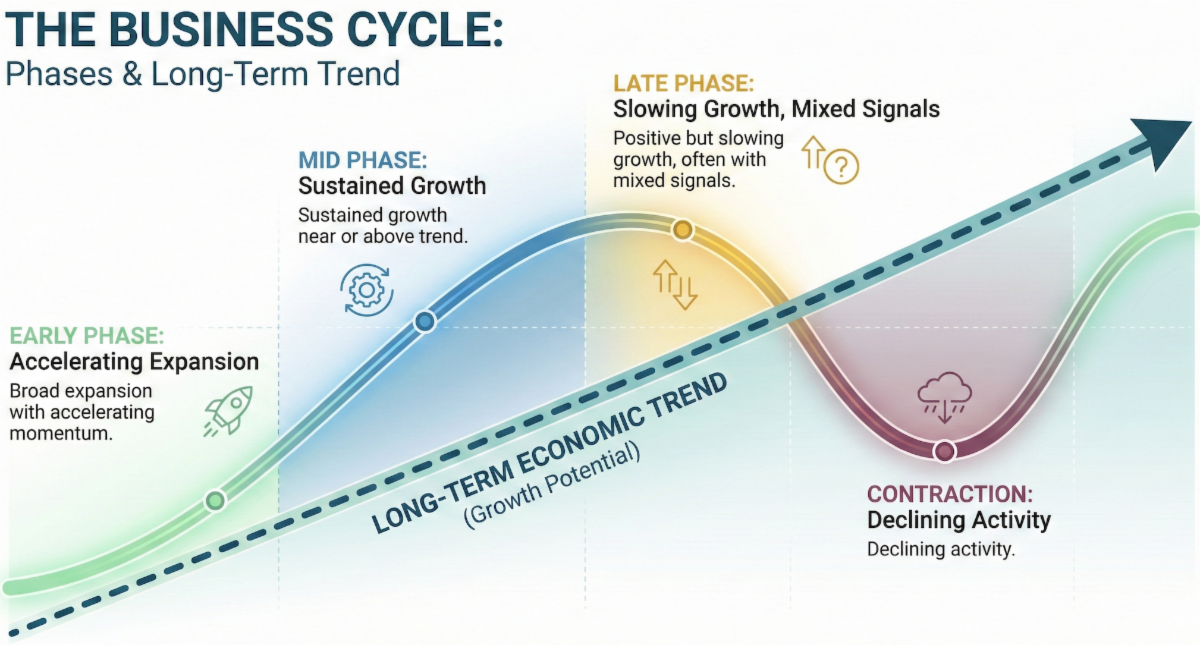

Global Business Cycles: Where We Stand

American investors tend to suffer from home bias, the tendency to overweight domestic investments in their portfolios. The US now accounts for roughly 65% of global stock market capitalization, but only about 26% of global GDP. That gap suggests US markets are expensive relative to what the economy actually produces.

I monitor economies across 10 regions beyond the US for two reasons. First, diversification: different economies move through business cycles at different speeds, creating opportunities when US valuations look stretched. Second, interconnection: what happens in Asia, Europe, and Latin America doesn't stay there. Trade flows, supply chains, and financial markets link these economies to American companies and workers.

The global picture right now: most major economies are grinding through late cycle, with manufacturing weakness widespread and services doing the heavy lifting. Canada and South Korea have tipped into contraction. The bright spot is Southeast Asia, the only region showing early-cycle momentum.

Here's what I'm seeing across each region.

United States: Late Phase

The US economy is grinding through late-cycle territory. Manufacturing has been in contraction for nine straight months, with the latest Institute for Supply Management (ISM) reading at 48.2 on a scale where anything below 50 signals contraction. Yet services keep chugging along at 52.6, which is why we're not calling this a recession. Factories are struggling with tariffs, weak orders, and cost pressures, while hospitals, restaurants, and professional services continue to expand.

Consumer sentiment is the most concerning signal. The Conference Board's confidence index plunged to 88.7, its lowest point since April. The expectations component has been flashing a recession warning for ten consecutive months.

The labor market tells a similar story. Unemployment has drifted up to 4.4%, a full percentage point above its cycle low. Job gains are averaging just 62,000 per month over the past three months.

The Federal Reserve has cut rates three times since September, bringing the fed funds rate down to 3.50%-3.75%. But the most recent meeting revealed deep divisions, and Powell's message was clear: they're "well positioned to wait and see."

I'd turn less optimistic if the services Purchasing Managers Index (PMI) slipped below 50 or the labor market continued to weaken.

Europe: Late Phase

Europe's economy has settled into late-cycle territory with some signs of life that weren't there earlier in the year. The composite PMI rose 1.6 points over three months, driven by services accelerating to an 18-month high of 53.6.

Manufacturing remains the weak link. German factories have struggled with soft demand, high energy costs, and US tariff headwinds. The manufacturing PMI has spent most of 2025 below 50, though the decline has stabilized. It's not recovery, it's just less bad.

The labor market remains remarkably tight at 6.4% unemployment, barely above its all-time low. This combination of weak industrial production alongside full employment is a textbook late-cycle signal.

The European Central Bank (ECB) has stopped cutting rates after eight cuts brought the deposit rate from 4% to 2%.

Key risks: A deeper US-EU trade conflict could tip manufacturing into sharper decline.

Japan: Late Phase

Japan's economy has entered late cycle, with conditions that have stabilized but show little momentum for improvement.

Manufacturing has contracted for five straight months as automakers and semiconductor producers grapple with weaker foreign demand. Even with a bilateral trade agreement that reduced US tariffs on Japanese autos from 27.5% to 15%, shipments to America continue to fall.

Services tell a different story. Restaurant traffic, retail, and business services continue expanding, supported by strong domestic consumption. This resilience has prevented a broader downturn, but it's not generating enough lift to pull manufacturing out of its slump.

The labor market has loosened. Unemployment ticked up to 2.6%, notably higher than the 2.3% recorded three months earlier. Job openings relative to applicants have fallen to their lowest since early 2022.

Bond markets are pricing in another Bank of Japan rate hike, likely pushing the policy rate to 0.75%, the highest since 1995.

Canada: Contraction

Canada is in contraction, and the momentum is getting worse. But there's an unusual split: the hard numbers look better than the mood.

Official statistics show an economy holding its ground. Industrial output is up modestly from a year ago. Exports are essentially flat. These aren't strong numbers, but they're not collapsing either.

Business surveys tell a different story. The composite PMI dropped to 44.9. The services PMI crashed from 50.5 to 44.3 in a single month, a 6.2-point plunge that ranks among the steepest declines outside of pandemic disruptions.

When hard data and surveys diverge like this, the surveys usually win within a couple of months. Surveys capture sentiment and forward intentions; official statistics measure what already happened.

The Bank of Canada recently cut rates and has since held steady. If services weakness persists, the Bank has room to cut again.

Australia: Mid Phase

Australia is in a classic mid-cycle spot. The economy is growing and forward-looking signals lean constructive, but momentum isn't screaming "boom."

Services are doing the heavy lifting, with activity consistently in expansion territory at 52.7. Manufacturing is more uneven at 51.6, bouncing back after a softer patch but not showing the same broad strength.

Trade is helping. Goods exports are running 11.3% above a year ago, which matters for a commodity exporter. The labor market has loosened a bit. Unemployment is at 4.3%, higher than the 3.5% low, giving businesses more breathing room on hiring and wages.

The Reserve Bank has been sitting tight, keeping the cash rate unchanged at 3.60% for the last few meetings.

What could change the picture: A sharp slowdown in China that hits commodity demand, or a renewed spike in inflation forcing tougher policy.

China: Mid Phase

China is sitting in mid-cycle territory, but momentum has clearly softened. The stock market rally that began in late 2024 has shown decent gains, but the initial burst of optimism has faded as economic data remain mixed.

Mainland Chinese stocks have outperformed their Hong Kong-listed counterparts, which typically means domestic investors are leaning into Beijing's policy support while foreign capital stays more cautious.

The currency picture is calm. The yuan has been essentially stable over the past three months, a notable improvement from earlier in the year when the dollar pushed above 7.35.

Where the tone has weakened is in business surveys. Private-sector PMI readings cooled, with manufacturing slipping back below 50 at 49.9 even as services kept expanding at 52.1. Beijing appears comfortable with this pace for now. The People's Bank of China (PBOC) hasn't touched rates since May, holding ammunition in reserve.

India: Late Phase

India is firmly in late-cycle territory with a deteriorating trajectory. The economy is running on fumes from an earlier acceleration.

The soft data still looks strong. Manufacturing and services PMIs are both comfortably in expansion territory at 56.6 and 59.8 respectively. But dig into the hard numbers and the picture shifts. Industrial production grew just 0.4% year-over-year in the latest reading, the weakest in over a year. Exports tell a more troubling story: recent merchandise shipments contracted nearly 12%, hammered by US tariffs.

What's keeping this from looking worse is the domestic consumer. With headline inflation at just 0.71%, Indian households have real purchasing power. The Reserve Bank of India (RBI) has continued its easing cycle, with its benchmark rate now at 5.25%.

The labor market is the clearest late-cycle signal. Unemployment at 5.2% sits just 0.3 percentage points above its three-year low.

Taiwan: Late Phase

Taiwan's economy is running hot on the outside but cooling on the inside, and that mismatch tells the real story.

The headline numbers look spectacular. Exports just posted their strongest month in over fifteen years, up 56% from last year, driven by insatiable global demand for AI chips and servers. Export orders are running 25% ahead of last year. Industrial production is growing at 14.5%.

But dig into manufacturing surveys and you get a more nuanced picture. Some PMI readings have shown weakness, with manufacturers reporting falling new orders and weak customer demand outside the tech sector.

Taiwan's economy has become a tale of two industries. The AI supply chain is booming, with Taiwan Semiconductor Manufacturing Company (TSMC) shipping advanced chips to Nvidia and Apple. But traditional manufacturing is struggling under tariff pressures.

The labor market confirms we're late in the cycle. Unemployment just hit a 24-year low at 3.33%.

South Korea: Contraction

South Korea's economy has tipped into contraction. Manufacturing has contracted for two straight months, with the PMI stuck at 49.4. The industrial sector took a brutal hit with output plunging 8.1% year-over-year.

The consumer picture is more worrying than headlines suggest. The Bank of Korea's sentiment index hit an eight-year high at 112.4, but actual retail spending hasn't kept pace. That's a classic late-cycle disconnect: people feel okay about the future but aren't opening their wallets.

What's preventing a sharper downturn? Exports, specifically semiconductors. Recent shipments grew 8.4% year-over-year, with chip exports surging nearly 39%.

The labor market tells an interesting story. Unemployment sits at 2.7%, meaning almost no slack left in the system. Manufacturing and construction jobs continue to shrink.

The Bank of Korea (BOK) has hit pause after cutting rates by a full percentage point since late 2024.

Latin America: Late Phase

Latin America is grinding through late-cycle with clear signs of fatigue. Business surveys have been weak overall, with services only just poking back above 50.

Brazil's labor market tells the most important story. Unemployment at 5.4%, the lowest on record, sounds great on the surface, but from a cycle perspective it means essentially no slack left. The Central Bank of Brazil (BCB) has kept rates parked at 15% for four straight meetings. Inflation expectations remain stuck above target at 4.4 - 4.5%.

The trade situation deserves attention. Brazil's exports grew 9.1% year-over-year recently, which masks a significant reshuffling: China-bound shipments surged 33% while US exports collapsed 20% after Washington slapped 50% tariffs on Brazilian goods.

The services sector just flipped back to expansion at 50.1, breaking a seven-month contraction streak.

ASEAN-5: Early Phase

Southeast Asia is the standout story. The ASEAN-5 economies (Indonesia, Malaysia, Philippines, Singapore, and Thailand) are the only region in early-cycle territory with an improving trajectory.

The manufacturing picture shows genuine strength. The three-month average PMI sits at 52.4, well into expansion territory, and momentum is accelerating. The latest reading of 53.0 marked the third-strongest improvement in over three years. Thailand is leading the charge, ranking among the top global performers.

Singapore's numbers are even more striking. Industrial production jumped 29.1% year-on-year, the strongest growth since 2010, driven by biomedical manufacturing and AI-related electronics. Non-oil domestic exports grew 22.2% as regional supply chains benefit from trade diversion patterns.

The one wrinkle is the labor market. Unemployment sits at just 2.0%, a late-cycle signal in an otherwise early-cycle picture.

Four of five major ASEAN central banks are in easing mode, providing a supportive backdrop.

Disclosure

This material is provided by Todd Van Der Meid, MBA, CFP®, through Rhino Wealth Management, Inc., a Registered Investment Adviser, solely for informational purposes. It is not intended as investment, tax, legal, or accounting advice. Investors should consult qualified professionals before making financial decisions.

Opinions expressed herein are general in nature and not tailored to individual circumstances. Investment strategies discussed may not be suitable for every investor. All investments carry risk, including possible loss of principal, and past performance does not guarantee future results. No investment strategy or risk management technique ensures profit or eliminates risk in all market conditions.

Investments in foreign or emerging markets involve additional risks, such as currency fluctuations, geopolitical instability, and varying accounting standards. Sector-specific investments can be more volatile due to their concentrated nature. References to indexes are for illustrative purposes; indexes are unmanaged, cannot be invested into directly, and their performance does not reflect fees, expenses, or sales charges. Index performance is not indicative of specific investment performance.

Economic forecasts and forward-looking statements reflect current views and assumptions and are subject to change. Actual results may vary materially due to market or other conditions. There is no obligation to update forward-looking information.

Information presented herein comes from reliable third-party sources but is not guaranteed for accuracy or completeness. Rhino Wealth Management, Inc. disclaims liability for errors or omissions. Portions of this content may be generated using advanced analytical tools, including artificial intelligence, and all such content has been reviewed and validated by Todd Van Der Meid, MBA, CFP®, using proprietary quality-control measures. Rhino Wealth Management, Inc. does not directly hold securities; however, securities mentioned may be included within recommended portfolio models or held by clients. Please refer to our Form ADV for additional details regarding potential conflicts of interest.