A Peace Deal and a Hawkish Fed, in the Same Week

A peace deal may reopen the Strait of Hormuz and ease oil-driven inflation, but the Fed is not ready to declare victory. Markets rose on the news, yet investor sentiment stayed cautious as higher-rate risk moved back into focus. The result is a week where the path to lower inflation looks clearer, but the Fed’s patience looks thinner.

More Red Arrows than Usual

Inflation moved the wrong way again in May. Consumer prices rose 4.2% over the past year, producer prices 6.5%, and jobless claims ticked up across the board. Growth is still tracking at 3.3%, yet markets now put roughly a 78% chance on a rate hike within the next year. All of it lands on the Fed's table when it meets next week. Here's the week's data at a glance.

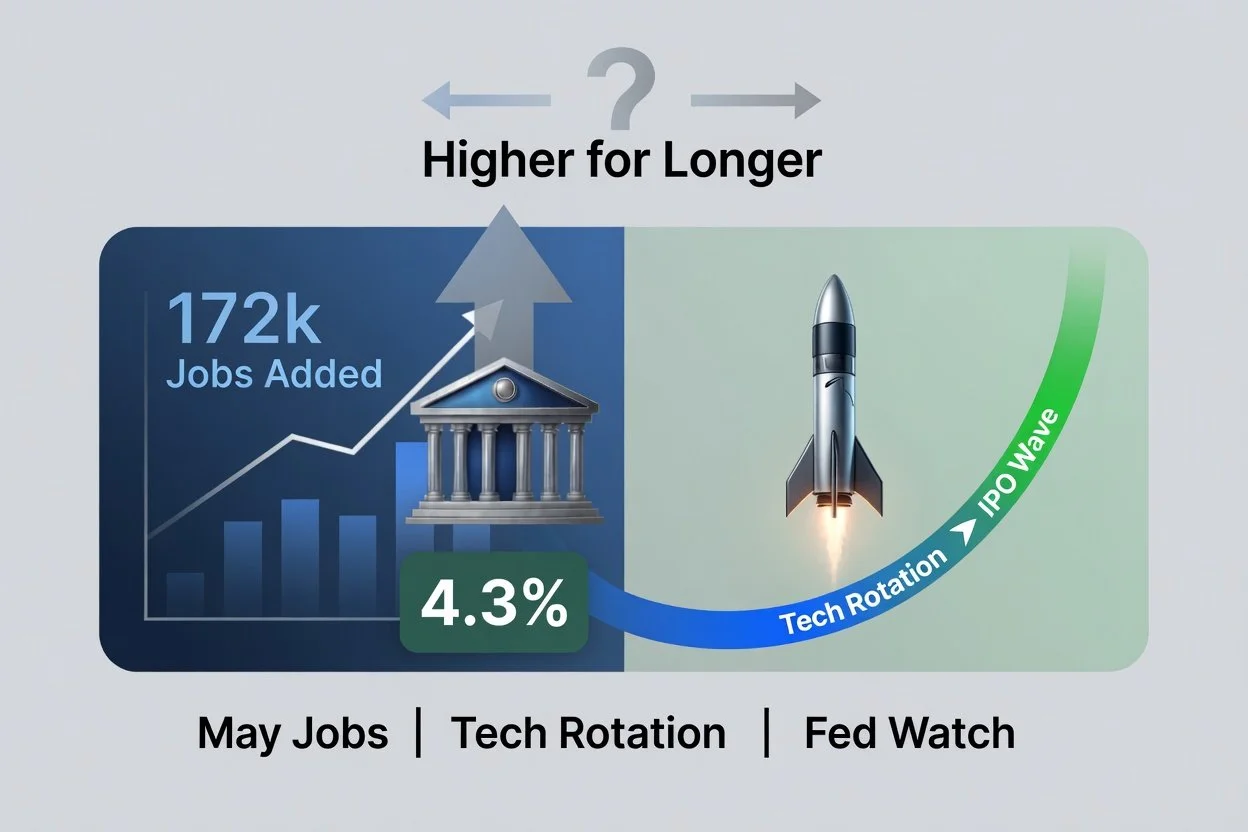

Jobs, Rates, and This Week's Selloff

A strong May jobs report has markets rethinking the path of interest rates, with a hike now looking more likely than a cut. Meanwhile, money is rotating out of technology stocks ahead of the SpaceX, Anthropic, and OpenAI IPOs. Here's what's driving markets this week and what I'm watching from here.