Growth Slows, Inflation Doesn't

The S&P 500 finished the week down 2.02% as investors weighed two competing messages. On one hand, the service side of the economy remained solid, jobless claims stayed contained, and productivity data was constructive. On the other, Friday's payroll report showed a clear loss of hiring momentum, unemployment moved higher, and the Atlanta Fed's GDPNow estimate for first-quarter growth moved lower, even as wage growth stayed firm and inflation signals remained uncomfortably sticky. Add in a sharp escalation in the Middle East and a jump in oil prices, and the market spent the week less focused on a soft landing and more focused on the risk of slower growth arriving before inflation is fully under control.

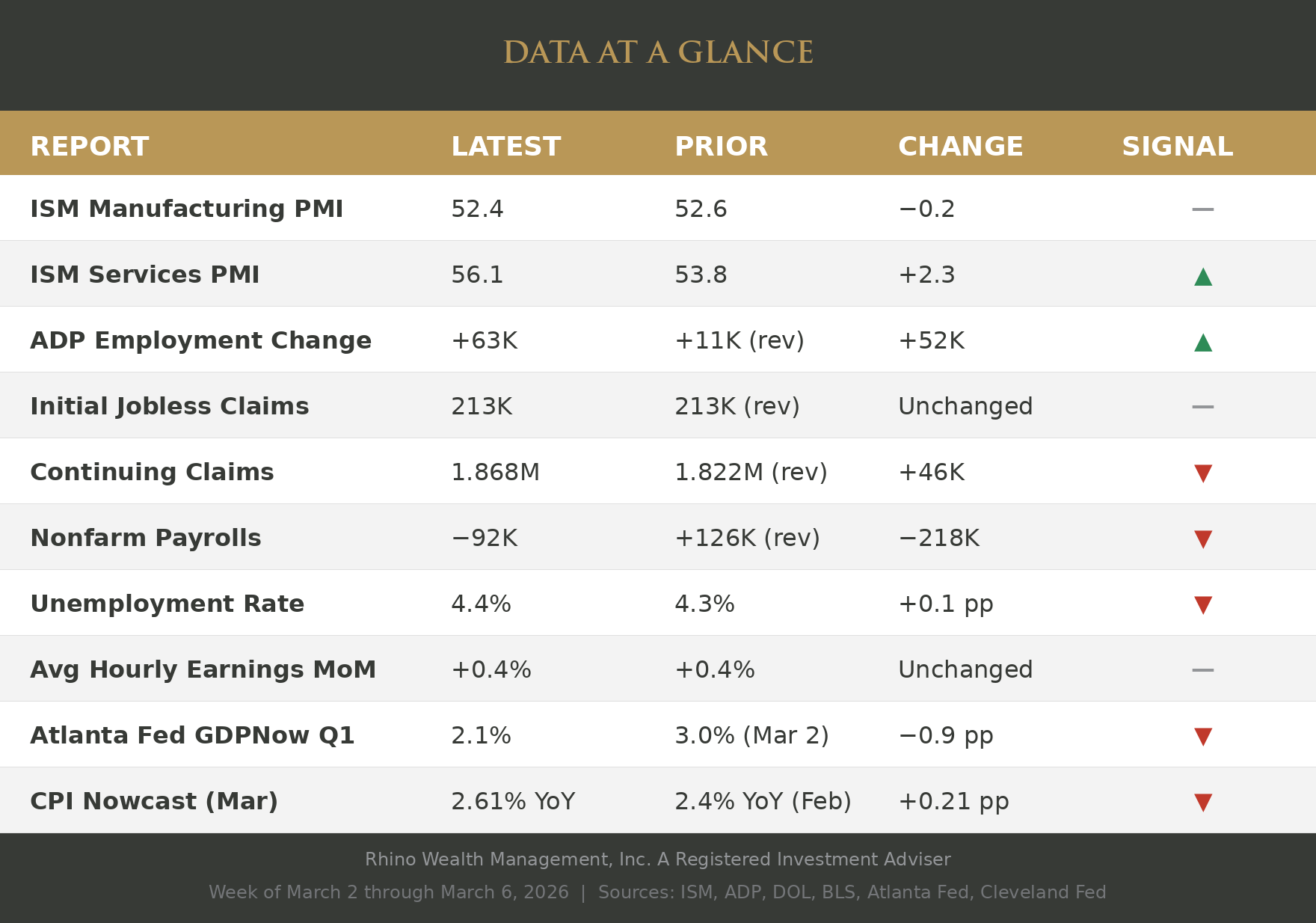

- ISM Manufacturing PMI — Survey of U.S. factory managers. Above 50 indicates expansion; below 50 indicates contraction. (Institute for Supply Management)

- ISM Services PMI — Same concept for the services sector, which makes up most of the U.S. economy. (Institute for Supply Management)

- ADP Employment Change — Monthly estimate of private-sector jobs added or lost, based on payroll data. Excludes government jobs. (ADP Research Institute)

- Initial Jobless Claims — Number of people filing for unemployment benefits for the first time that week. Lower levels generally indicate fewer layoffs. (U.S. Department of Labor)

- Continuing Claims — Total number of people still receiving unemployment benefits. Rising levels can indicate it is taking longer for people to find new work. (U.S. Department of Labor)

- Nonfarm Payrolls — Headline figure from the government’s monthly jobs report, showing the total number of jobs added or lost across the economy. (Bureau of Labor Statistics)

- Unemployment Rate — Percentage of the labor force that is actively looking for work but does not have a job. (Bureau of Labor Statistics)

- Average Hourly Earnings MoM — Month-over-month change in average wages. Steady growth is healthy; excessively rapid growth can add to inflation pressure. (Bureau of Labor Statistics)

- Atlanta Fed GDPNow (Q1) — Real-time model estimate of how fast the economy is growing this quarter. It is not an official forecast. (Federal Reserve Bank of Atlanta)

- CPI Nowcast (March) — Daily estimate of the Consumer Price Index, a common measure of inflation, showing where prices may be headed before the official report. (Federal Reserve Bank of Cleveland)

The geopolitical shock came first. After the weekend strikes involving the U.S., Israel, and Iran, markets quickly shifted to the risk of broader disruption across the region. Threats to shipping through the Strait of Hormuz, a pullback in war-risk insurance, and a sharp move higher in crude all reinforced the same concern: this was no longer just a headline risk. With roughly a fifth of global oil consumption moving through that corridor, any sustained disruption would have direct consequences for energy prices, transportation costs, and the inflation outlook.

Then Friday's jobs report added a second layer of concern. The economy lost 92,000 jobs in February, the unemployment rate rose to 4.4%, and prior months were revised lower. Some of that weakness may reflect temporary factors, but the broader message was still clear. Hiring has slowed, growth expectations are softening, and the labor market no longer looks like the reliable source of resilience it did a few months ago.

Markets have been through versions of this before. The initial response to geopolitical conflict is usually a move away from risk, but the lasting impact depends on whether the event remains contained or spills into oil, trade, and growth. If the conflict stays limited, markets may eventually stabilize. If it evolves into a prolonged energy shock, the economic consequences become harder to ignore.

There were still a few encouraging signs. ISM Services stayed firmly in expansion territory, productivity was revised higher, and initial claims remained low enough to suggest layoffs are not yet accelerating. But those positives were offset by average hourly earnings holding at 0.4% month over month and the Cleveland Fed's March CPI nowcast moving higher. In other words, inflation is still proving stubborn at the same time growth looks more fragile.

Growth may be slowing, but inflation may not be easing fast enough to give the Fed much room to respond. That tension defined the week, and it's likely to define the weeks ahead.