Playing Defense: The Economy Isn't Breaking, It's Bracing

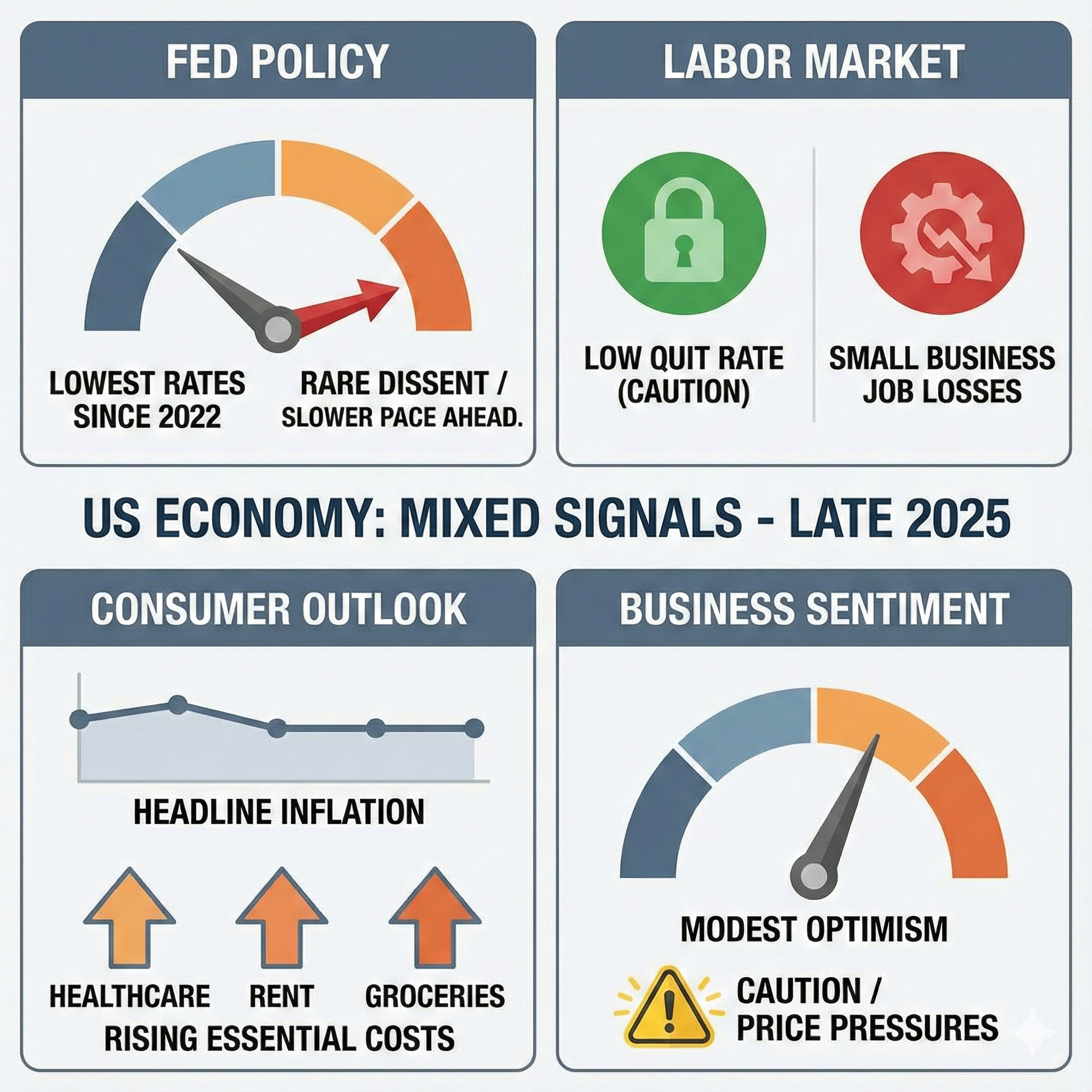

The economy is sending mixed signals as 2025 winds down. The Fed delivered its third consecutive rate cut this month, bringing rates to their lowest level since 2022, but the decision drew rare dissent, and officials are signaling a slower pace ahead.

The labor market tells two different stories, depending on where you look. Weekly jobless claims showed holiday-related volatility, and small businesses shed jobs at the fastest pace since 2023. At the same time, workers who are employed are holding on tightly. The quit rate has fallen to a four-year low, a clear sign of caution rather than confidence.

Consumers echo that tension. Inflation expectations remain contained overall, but households are bracing for sharper increases in the costs that matter most: healthcare, rent, and groceries.

This is an economy that is not breaking down but not firing on all cylinders either. Growth expectations are modest, caution is widespread, and both businesses and workers appear to be playing defense heading into the new year. After weeks of limited government data, the releases are starting to flow again. Here's what stood out in the private and government data this week.

Survey of Consumer Expectations

The New York Fed's November survey shows overall inflation expectations holding steady at 3.2% for one year out and 3.0% for three- and five-year horizons. But beneath that calm surface, consumers expect sharper price increases in specific categories: medical care expectations hit their highest level since 2014 at 10.1%, rent jumped to 8.3%, and food costs are expected to rise 5.9%. The disconnect between stable headline expectations and rising category-specific concerns suggests Americans are bracing for continued pressure on everyday essentials even as broader inflation stabilizes.

Source: Federal Reserve Bank of New York (2025) Survey of Consumer Expectations: November 2025. New York: Federal Reserve Bank of New York.

National Federation of Independent Business (NFIB) Small Business Optimism Index

Small business optimism ticked up slightly in November, with the NFIB index reaching 99, its highest level in three months. The data shows a mixed picture: sales expectations jumped significantly and more owners rated their business health as "good," but inflation pressures are clearly building, with 34% of owners raising prices, the highest since March 2023. Labor quality remains the top concern for about one in five owners, though that's improved from October. The bottom line: small businesses are feeling somewhat better about current conditions, but they're passing costs to customers and remain cautious about the road ahead.

Source: National Federation of Independent Business (2025) NFIB Small Business Optimism Index: November 2025. Nashville, TN: NFIB Research Center.

ADP® National Employment Report

ADP Research, the nation's largest private payroll processor, produces both monthly employment reports and a newer weekly jobs tracker. Their weekly data showed US private employers added an average of 4,750 jobs per week in the four weeks ending November 22, 2025, following three consecutive periods of declines. This suggests job losses eased in mid-November. However, ADP's official November monthly report showed a decline of 32,000 jobs, the largest monthly drop since March 2023, driven primarily by a 120,000-job loss at small businesses.

Source: Automatic Data Processing, Inc. (2025) ADP National Employment Report: November 2025. Roseland, NJ: ADP Research Institute.

Job Openings and Labor Turnover Summary

Job openings held essentially flat at 7.67 million, a modest 12,000 increase from September. The real story is the quits rate, which dropped to 1.8%, its lowest level since August 2020. Workers are staying put: voluntary departures fell by 187,000 to 2.94 million, with sharp declines in accommodation, food services, and healthcare. This signals reduced worker confidence in finding better opportunities elsewhere, a notable shift from the tight labor market conditions of recent years.

Source: U.S. Bureau of Labor Statistics (2025) Job Openings and Labor Turnover Summary: October 2025. Washington, DC: U.S. Department of Labor.

Federal Open Market Committee (FOMC) Meeting

The Fed cut rates by 25 basis points at its December meeting, bringing the target range to 3.5 to 3.75 percent. This marked the third consecutive reduction and the lowest level since 2022. The decision was contentious, with three dissenting votes for the first time since September 2019. Policymakers signaled only one additional 25 basis point cut in 2026, suggesting a slower pace of easing ahead. The Fed also announced it will begin purchasing Treasury bills on December 12, initially at a pace of $40 billion, to maintain adequate reserve levels following the end of quantitative tightening on December 1. Some observers view this as quantitative easing by another name, though Chair Powell characterized the purchases as technical operations designed to manage reserves and maintain control of the policy rate rather than provide economic stimulus.

The economic outlook improved modestly. GDP growth projections increased to 1.7 percent for 2025 and 2.3 percent for 2026, while PCE inflation expectations declined to 2.9 percent this year and 2.4 percent next year. Unemployment forecasts were unchanged at 4.5 percent for 2025 and 4.4 percent for 2026.

Source: Board of Governors of the Federal Reserve System (2025) Federal Reserve issues FOMC statement, 10 December. Washington, DC: Federal Reserve.

Unemployment Insurance

Initial jobless claims jumped 44,000 to 236,000 for the week ending December 6, 2025, the largest weekly increase since March 2020. This spike followed the Thanksgiving holiday week, when claims had dropped to their lowest level in over three years. Holiday-related volatility typically distorts weekly figures during this period. Meanwhile, continuing claims fell to 1.838 million, the lowest since mid-April 2025, suggesting the underlying labor market remains relatively stable despite the headline increase in new filings.

U.S. Department of Labor (2025) Unemployment Insurance Weekly Claims, December 6. Washington, D.C.: U.S. Department of Labor.

Disclosure

This material is provided by Todd Van Der Meid, MBA, CFP®, through Rhino Wealth Management, Inc., a Registered Investment Adviser, solely for informational purposes. It is not intended as investment, tax, legal, or accounting advice. Investors should consult qualified professionals before making financial decisions.

Opinions expressed herein are general in nature and not tailored to individual circumstances. Investment strategies discussed may not be suitable for every investor. All investments carry risk, including possible loss of principal, and past performance does not guarantee future results. No investment strategy or risk management technique ensures profit or eliminates risk in all market conditions.

Investments in foreign or emerging markets involve additional risks, such as currency fluctuations, geopolitical instability, and varying accounting standards. Sector-specific investments can be more volatile due to their concentrated nature. References to indexes are for illustrative purposes; indexes are unmanaged, cannot be invested into directly, and their performance does not reflect fees, expenses, or sales charges. Index performance is not indicative of specific investment performance.

Economic forecasts and forward-looking statements reflect current views and assumptions and are subject to change. Actual results may vary materially due to market or other conditions. There is no obligation to update forward-looking information.

Information presented herein comes from reliable third-party sources but is not guaranteed for accuracy or completeness. Rhino Wealth Management, Inc. disclaims liability for errors or omissions. Portions of this content may be generated using advanced analytical tools, including artificial intelligence, and all such content has been reviewed and validated by Todd Van Der Meid, MBA, CFP®, using proprietary quality-control measures. Rhino Wealth Management, Inc. does not directly hold securities; however, securities mentioned may be included within recommended portfolio models or held by clients. Please refer to our Form ADV for additional details regarding potential conflicts of interest.