The Fed Can See It, Too

The S&P 500 closed the week at 6506, marking its fourth consecutive weekly decline and breaking below its 200-day moving average for the first time since 2024. The index briefly rallied early in the week on hopes the Fed might signal rate cuts, but those hopes didn't survive Wednesday's Fed meeting as the Fed held rates steady and some members expressed increased risks to a weaker labor market as well as the potential for higher inflation. For all the fear and volatility, the S&P 500 is still only a little more than 7% off its all-time high. Even after the decline, the index is still trading in the mid-20s on a trailing price-to-earnings basis, well above its long-term average near 20. The market has gotten cheaper, but it hasn't gotten cheap.

In an ordinary week, the FOMC decision, a new Summary of Economic Projections, and a press conference from Chair Powell would be the lead story. This is not an ordinary week. The war in Iran continues to dominate the economic outlook, and it is increasingly shaping the data itself. What makes this week different from the last few is that the pipeline inflation pressures are no longer theoretical. They're showing up in the numbers.

Glossary

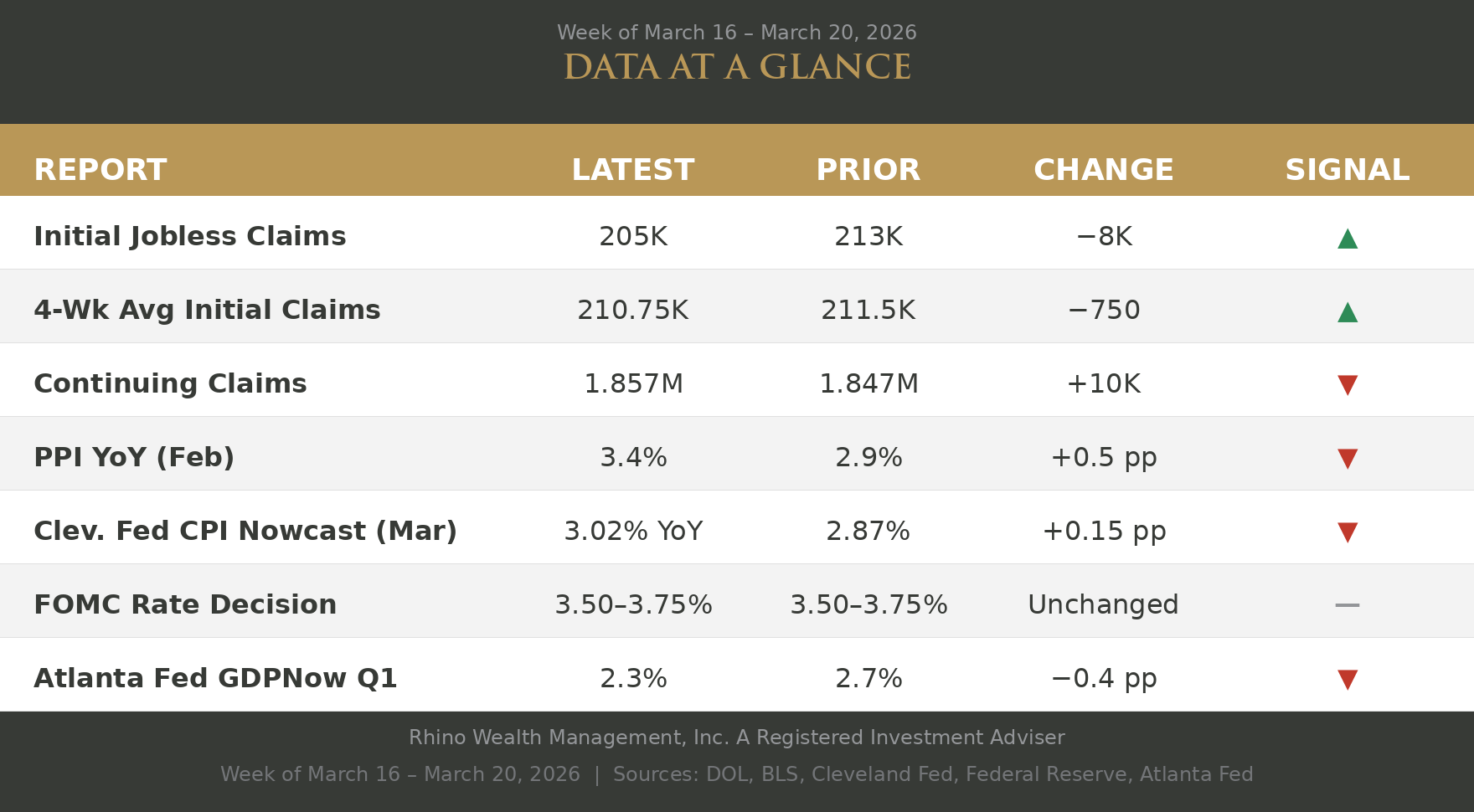

- Initial Jobless Claims -- Number of people filing for unemployment benefits for the first time that week. Lower levels generally indicate fewer layoffs. (U.S. Department of Labor)

- 4-Week Average Initial Claims -- A smoothed average of the last four weeks of initial claims, which reduces week-to-week noise and gives a clearer picture of the layoff trend. (U.S. Department of Labor)

- Continuing Claims -- Total number of people still receiving unemployment benefits. Rising levels can indicate it is taking longer for people to find new work. (U.S. Department of Labor)

- PPI YoY (Feb) -- The Producer Price Index measures year-over-year changes in prices received by domestic producers for their output. It is a gauge of wholesale inflation and can signal where consumer prices may be headed. (Bureau of Labor Statistics)

- Cleveland Fed CPI Nowcast -- A daily model estimate of where the Consumer Price Index is tracking for the current month before the official report is released. Rising readings suggest inflation pressure may be building. (Federal Reserve Bank of Cleveland)

- FOMC Rate Decision -- The Federal Open Market Committee's target range for the federal funds rate, which influences borrowing costs across the economy. The committee held rates steady at this meeting. (Federal Reserve)

- Atlanta Fed GDPNow Q1 -- A real-time model estimate of how fast the economy is growing in the current quarter. It updates frequently as new data is released. It is not an official forecast. (Federal Reserve Bank of Atlanta)

Last week I wrote that the rearview mirror looked okay but the windshield was foggier. This week, the fog is starting to clear, and what's coming into view is not especially reassuring.

Start with inflation, because that's where the story begins. Wednesday morning's Producer Price Index, which measures prices at the wholesale level before they reach consumers, came in at 3.4% year over year. That was the highest reading in a year, and it wasn't driven by one category. Food, fuel, and services all pushed higher at the same time. When wholesale inflation is this broad-based, it tends to show up in consumer prices a few months later. Meanwhile, the Cleveland Fed's CPI Nowcast, which estimates where consumer inflation is heading in real time, crossed 3% for March. A week ago it was closer to 2.9%. February's official CPI was 2.4%. The gap between where inflation was and where it's going is widening, and it's widening fast.

Inflation has now been running above the Fed's 2% target for five years with no relief in sight. The war in Iran will continue to put upward pressure on energy prices, but unlike the oil crisis of the 1970s, the United States now produces more oil and petroleum products than it consumes. Rising oil prices hurt at the pump, and nobody enjoys paying more for gasoline. But they also benefit American energy producers, which supports jobs and tax revenue in ways that didn't exist fifty years ago. The pain is real, but so is the offset. How this plays out depends largely on how long the conflict lasts. If it ends quickly, the energy shock fades. If it drags on, the inflation math gets harder.

That was the backdrop when the Fed announced its decision Wednesday afternoon. No surprise: rates stayed at 3.50-3.75%. But the details underneath told a more complicated story. The Fed's own projections now call for higher inflation this year than they expected three months ago. Several officials now see no rate cuts at all in 2026. And Chair Powell, in his press conference, offered very little in the way of direction, saying only that it's too soon to know how the conflict in the Middle East will affect the economy. The market read that as the Fed having no clear plan, and stocks sold off through the end of the week.

The Fed is stuck. It sees a labor market that's weakening but not yet critical. It sees inflationary forces building but recognizes the war could end as quickly as it began, which could ease price pressures on its own. Neither side of the picture is urgent enough to force a move. So for the second straight meeting, the Fed chose to wait.

The employment data continues to follow the same theme. Weekly jobless claims fell to 205,000, the lowest since January. Employers are not laying off in mass. But those who are out of work are finding it harder to land somewhere new. Continuing claims ticked higher again, and the unemployment rate has been slowly creeping up. It's a slow-hire, slow-fire labor market.

This is worth putting in broader context. Most of us grew up in a time when job growth was the single most important measure of a healthy economy. The economy needed to create jobs, lots of them, to absorb the baby boom generation and a growing population. That world is changing. The baby boomers are quickly retiring and our population isn't growing the way it used to. Over time, we will be settling into a new normal of slower job growth and higher productivity. That doesn't mean the economy is failing. It means the benchmarks we're used to measuring it by are shifting.

Meanwhile, the Atlanta Fed's real-time estimate of first-quarter GDP growth fell to 2.3%, down from 2.7% the week before. The economy is still growing, but the pace is coming down. That creates the tension that will define the next few months: prices are rising faster, growth is cooling, and the Fed is stuck in between. Cutting rates could make inflation worse. Holding rates could let the economy weaken further. Neither path is clean.

That's why the title of this week's note is what it is. The Fed can see the same thing the rest of us can. Inflation is reaccelerating. Growth is fading. And the tools they have to address one side of the problem risk making the other side worse. For now, they're choosing to wait. The question is how long that remains a viable option.

I'm watching this closely.