The Illusion of Growth: How AI Investment Is Masking Economic Weakness

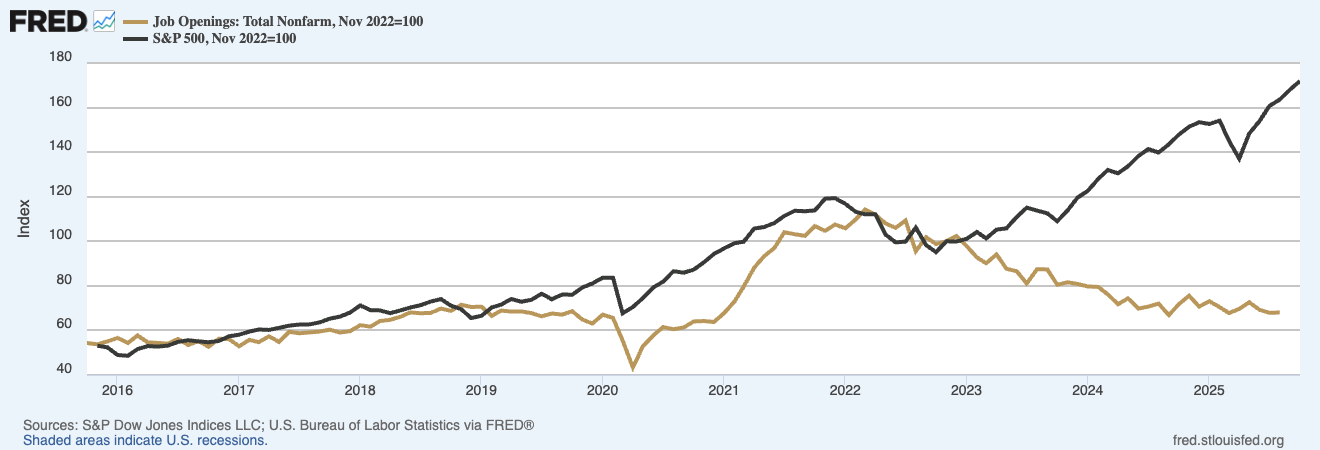

A graph has been circulating on social media titled "The Scariest Chart." Originally posted by First Trade, it plots two lines that tell what appears to be a devastating story: since November 2022, the S&P 500 has surged roughly 64% while job openings have dropped nearly 40%.

The timing seems damning. ChatGPT launched in November 2022. The implication feels obvious—AI is enriching investors while devastating workers. But the real story is more concerning: the economy's apparent strength is increasingly an illusion created by a tiny sliver of AI-related activity, while the broader economy contracts beneath the surface.

What's Actually Driving GDP

Harvard economist Jason Furman recently quantified something extraordinary: AI infrastructure investments—specifically data centers and information-processing equipment—accounted for 92% of U.S. GDP growth in the first half of 2025, despite representing only 4% of total GDP.¹ Strip out those technology investments, and GDP growth would have been essentially flat at just 0.1% annualized.²

This isn't normal economic expansion. This is one sector carrying the entire statistical appearance of growth while the rest of the economy treads water.

The Real Economy Tells a Different Story

While equity markets grind higher on AI euphoria, high-frequency freight data reveals what's actually happening in the physical economy. FreightWaves data shows outbound freight volumes down 18% year-over-year, with long-haul trucking collapsed 30%.³ Local distribution remains flat—consumers are still buying essentials—but manufacturing, automotive, and housing segments are under significant pressure.

The divergence is stark. The hyperscalers—massive cloud computing companies like Amazon, Microsoft, and Google that operate data centers at enormous scale—employ roughly 2 million Americans and move minimal freight. Manufacturing, transportation, and industrial sectors employ 35 million workers and are showing recession-level contraction in activity.³

Freight has historically been a leading indicator. When trucks stop rolling, it's because factories aren't producing and warehouses aren't restocking. The goods economy isn't slowing—it's already contracted.

The Job Market Isn't About AI Yet

Job openings peaked at 12.1 million in March 2022—eight months before ChatGPT's debut.⁴ That same month, the Federal Reserve began raising interest rates for the first time in over three years, launching an aggressive campaign that would see eleven rate hikes through July 2023.⁵

The Fed's explicit goal was to cool the economy by making borrowing more expensive, reducing investment, and slowing hiring. That's what happened. Job openings fell to 7.18 million by August 2025.⁴ As the Fed raised rates, the economy and demand for labor slowed.

If AI were the primary culprit, the tech sector should show the steepest decline in job openings. Data from Employ America reveals the opposite.⁶ The Information sector had the smallest drop in job postings. The largest declines came from construction (down nearly 40% year-over-year by late 2024), manufacturing, and energy extraction—sectors hammered by higher interest rates, not automation.⁷

Market Concentration Creates Fragility

While the underlying economy weakens, AI-related stocks have driven nearly all market gains. According to JPMorgan, AI-linked companies—including Nvidia, Microsoft, Apple, Amazon, Alphabet, and Meta—now represent roughly 47% of the S&P 500's total value.⁸ These stocks accounted for 75% of the index's returns and 80% of earnings growth since late 2022, generating approximately $5 trillion in household wealth gains.⁸

The Magnificent Seven now make up more than one-third of the S&P 500, exceeding even the concentration seen during the dot-com bubble.⁹ This creates a dangerous setup: statistical GDP growth driven by one narrow sector, equity market performance driven by seven companies, and an underlying economy that's already contracting in key industrial segments.

A Different Kind of Divergence

Historically, job openings and stock market performance moved together for over two decades of JOLTS data.¹⁰ When the economy strengthened, companies posted more jobs and stock prices rose. When conditions weakened, both declined in tandem.

This divergence is unprecedented—and it matters because of what's driving it. The dot-com bubble offers context but not comfort. When it burst in 2000, the NASDAQ lost 78% of its value.¹¹ Yet the subsequent recession was remarkably mild. GDP declined less than 1% cumulatively, and unemployment peaked at 6.3%.¹² The damage was largely contained to the stock market and technology sector.

Today's situation may be more concerning. The dot-com crash preceded economic weakness. This time, much of the underlying economy is already showing contraction in labor demand and production activity. The stock market's strength isn't leading a robust economy—it's diverging from one that's already cooling.

Early AI Impact Is Beginning to Show

The labor market weakness tells us more about the Fed's success in slowing economic activity than about technology displacing workers at scale—at least for now. But early signals suggest AI is beginning to affect certain job categories. Research from Stanford shows younger workers in AI-heavy fields have seen employment drop 13% relative to other groups since generative AI became widespread.¹³ By March 2024, college graduate unemployment reached 5.8%—a four-year high.¹⁴

What Happens When the Illusion Breaks

The economy appears to be growing based on one narrow category of investment. The stock market appears strong based on a small subset of companies' valuations. Freight volumes, job openings in goods-producing sectors, and GDP excluding AI infrastructure all tell a story of contraction or stagnation.

If AI stocks are experiencing a valuation bubble, the divergence will eventually close. That convergence could happen in two ways: stock prices fall to meet economic reality, or the underlying economy reaccelerates as AI investments drive broader productivity gains.

Given current conditions—concentrated equity risk, weakness in rate-sensitive and goods-producing sectors, and GDP growth dependent on a single category of investment—the path of least resistance may be downward for stock prices rather than upward for the broader economy.

The 2001 recession was mild because the damage was mostly financial. If we're heading into a period where an equity market correction meets an already-weakening physical economy, the impact could be more broadly felt.

What This Means for Investors

The concentration risk is real and measurable. When 47% of an index's value rests with a handful of AI-focused companies, and those companies' investments represent 92% of GDP growth, vulnerability increases dramatically. These companies are priced for perfection, assuming AI infrastructure investments will generate returns that justify current valuations.

The K-shaped economy creates both risks and opportunities for portfolio positioning. Services and tech are carrying the load while goods production deteriorates. The critical question is how long that can continue before the divergence resolves.

The Bottom Line

"The Scariest Chart" is scary for real reasons—just not the ones that first appear. It doesn't show AI destroying the economy. It shows an economy whose apparent strength is increasingly an illusion created by concentrated AI investment, while the physical economy beneath that statistical veneer is already contracting.

The real risk isn't that AI has already fractured the economy. It's that we're mistaking narrow investment activity for broad economic health. When that illusion breaks—as unprecedented divergences eventually do—it may not be the gentle correction of an isolated tech bubble. It could be a broader reckoning where falling stock prices meet an economy that's already weakened.

For investors, this means looking beyond headline index performance and GDP figures to understand what's actually driving returns and what happens when historically unprecedented divergences inevitably narrow.

References

- Furman, J. (2025) Analysis of AI infrastructure impact on U.S. GDP growth, first half 2025. Available at: https://x.com/jasonfurman/status/1971995367202775284 (Accessed: 3 November 2025).

- Fortune (2025) 'Data centers and GDP growth: Without AI investment, U.S. economy barely grew in H1 2025'. Available at: https://fortune.com/2025/10/07/data-centers-gdp-growth-zero-first-half-2025-jason-furman-harvard-economist/ (Accessed: 3 November 2025).

- FreightWaves (2025) High-frequency freight data and economic indicators. Available at: https://www.freightwaves.com (Accessed: 3 November 2025).

- U.S. Bureau of Labor Statistics (2025) Job Openings and Labor Turnover Survey (JOLTS). Available at: https://www.bls.gov/jlt/ (Accessed: 3 November 2025).

- Board of Governors of the Federal Reserve System (2023) Federal Reserve issues FOMC statement. Available at: https://www.federalreserve.gov/newsevents/pressreleases/monetary20230726a.htm (Accessed: 3 November 2025).

- Thompson, D. (2024) 'Is This the New "Scariest Chart in the World"?', The Atlantic (Substack). Available at: https://www.derekthompson.org/p/is-this-the-new-scariest-chart-in (Accessed: 3 November 2025).

- Mui, P. (2024) Employ America Analysis: Sectoral Job Openings Data. Employ America. Available at: https://www.employamerica.org (Accessed: 3 November 2025).

- J.P. Morgan (2024) AI Stocks and Market Concentration Analysis. J.P. Morgan Research.

- Shalett, L. (2024) Magnificent Seven Market Concentration. Morgan Stanley Wealth Management Research.

- U.S. Bureau of Labor Statistics (2002-2025) Job Openings and Labor Turnover Survey Historical Data. Available at: https://www.bls.gov/jlt/ (Accessed: 3 November 2025).

- NASDAQ (2002) NASDAQ Composite Index Historical Data. Available at: https://www.nasdaq.com (Accessed: 3 November 2025).

- National Bureau of Economic Research (2003) Business Cycle Dating. Available at: https://www.nber.org/research/business-cycle-dating (Accessed: 3 November 2025).

- Autor, D. et al. (2024) The Impact of Generative AI on Young Workers. Stanford University Digital Economy Lab.

- U.S. Bureau of Labor Statistics (2024) Current Population Survey: Unemployment by Educational Attainment. Available at: https://www.bls.gov/cps/ (Accessed: 3 November 2025).

Disclosure

This material is provided by Todd Van Der Meid, MBA, CFP®, through Rhino Wealth Management, Inc., a Registered Investment Adviser, solely for informational purposes. It is not intended as investment, tax, legal, or accounting advice. Investors should consult qualified professionals before making financial decisions.

Opinions expressed herein are general in nature and not tailored to individual circumstances. Investment strategies discussed may not be suitable for every investor. All investments carry risk, including possible loss of principal, and past performance does not guarantee future results. No investment strategy or risk management technique ensures profit or eliminates risk in all market conditions.

Investments in foreign or emerging markets involve additional risks, such as currency fluctuations, geopolitical instability, and varying accounting standards. Sector-specific investments can be more volatile due to their concentrated nature. References to indexes are for illustrative purposes; indexes are unmanaged, cannot be invested into directly, and their performance does not reflect fees, expenses, or sales charges. Index performance is not indicative of specific investment performance.

Economic forecasts and forward-looking statements reflect current views and assumptions and are subject to change. Actual results may vary materially due to market or other conditions. There is no obligation to update forward-looking information.

Information presented herein comes from reliable third-party sources but is not guaranteed for accuracy or completeness. Rhino Wealth Management, Inc. disclaims liability for errors or omissions. Portions of this content may be generated using advanced analytical tools, including artificial intelligence, and all such content has been reviewed and validated by Todd Van Der Meid, MBA, CFP®, using proprietary quality-control measures. Rhino Wealth Management, Inc. does not directly hold securities; however, securities mentioned may be included within recommended portfolio models or held by clients. Please refer to our Form ADV for additional details regarding potential conflicts of interest.