The Supreme Court Just Rewrote the Tariff Playbook

A quick note: much of this week's data reflects Q4 2025 and was delayed by the October-November government shutdown. That same shutdown also left its mark on the numbers themselves, shaving roughly a full percentage point off GDP growth. With that context, the big picture is a mixed bag. The labor market is holding up well on the hiring side, but job seekers are facing longer searches once they're out of work. Inflation is the story to watch: it's moving in the wrong direction at exactly the wrong time, likely keeping the Fed on the sidelines longer than markets would like. Consumers are still spending but showing early signs of pulling back, while housing and business investment both surprised to the upside with strong December rebounds. The overall picture is an economy that's cooling but not cracking, with inflation as the primary wildcard for the months ahead.

The most consequential story this week landed just hours before the market closed. The Supreme Court struck down President Trump's sweeping tariffs in a 6-3 ruling, finding that the International Emergency Economic Powers Act (IEEPA) does not authorize the president to impose import duties without Congress. Chief Justice Roberts wrote the majority opinion, joined by two Trump-appointed justices, Gorsuch and Barrett, along with the three liberal justices. President Trump called the ruling "deeply disappointing," then immediately announced a new 10% global tariff under a different legal authority that can remain in place for up to 150 days without congressional approval.

Markets rallied on the news. Attention is already turning to whether the government will be required to refund an estimated $130 billion or more in tariffs already collected under IEEPA. The court's opinion was silent on refunds, which likely means years of additional litigation. The tariff landscape has shifted, but it hasn't disappeared. Tariffs imposed under other authorities, including those on steel, aluminum, and automobiles, remain in effect.

Labor Market

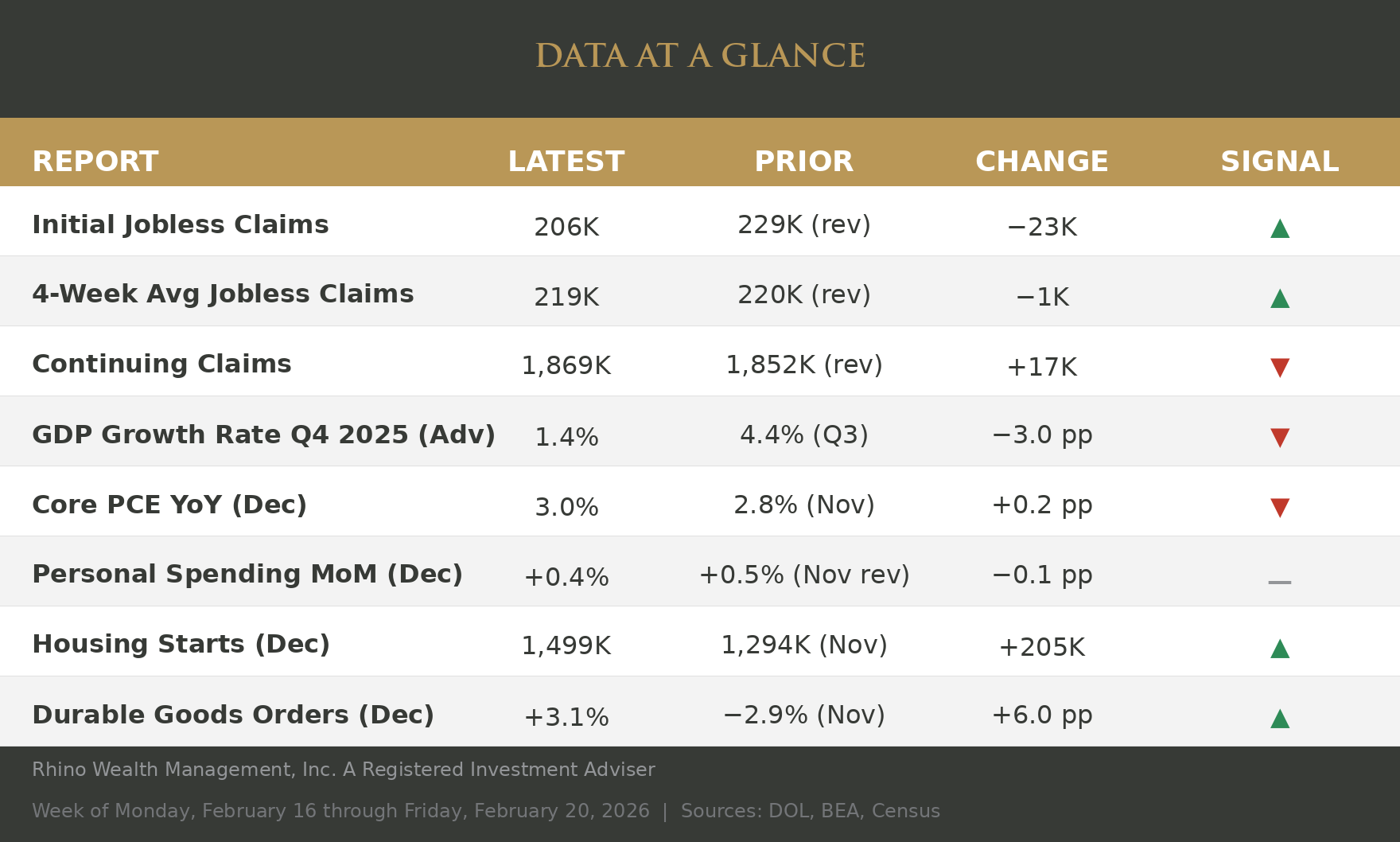

- Initial Jobless Claims (206K): New filings for unemployment benefits dropped by 23,000 from the prior week, one of the lowest readings in recent months. The labor market continues to hold firm.

- 4-Week Average Jobless Claims (219K): The four-week moving average, which smooths out week-to-week noise, ticked down to 219K. The downward trend in new filings is holding.

- Continuing Claims (1,869K): The number of people still collecting unemployment benefits rose by 17,000. Fewer workers are losing jobs, but those who are unemployed appear to be taking slightly longer to find new positions.

Growth

- Gross Domestic Product (GDP) Growth Rate Q4 2025 (Advance Estimate, 1.4%): The economy grew at a 1.4% annualized rate in Q4, a notable slowdown from the 4.4% pace in Q3. The deceleration was driven by declines in government spending and exports. The Bureau of Economic Analysis estimates that the October–November government shutdown alone shaved roughly 1.0 percentage point off the quarter's growth.

Inflation

- Core Personal Consumption Expenditures (PCE): The Fed's preferred inflation measure rose to 3.0% year-over-year in December, up from 2.8% in November and further from the 2% target. This is the highest reading since mid-2024 and may reinforce the Fed's cautious stance on rate cuts.

Consumer

- Personal Spending MoM: Consumer spending grew 0.4% in December, a slight step down from the revised 0.5% gain in November. Spending remains positive, but the slowdown, paired with a personal saving rate of just 3.6%, suggests consumers may be settling into a more cautious pace heading into 2026.

Housing & Manufacturing

- Housing Starts: Housing starts jumped to a 1,499K annualized rate, up 205K from November's 1,294K. The rebound in new residential construction signals renewed builder confidence, even with mortgage rates still elevated.

- Durable Goods Orders: Orders for long-lasting manufactured goods (things like appliances, machinery, and vehicles) swung from a 2.9% decline in November to a 3.1% gain in December, a 6.0 percentage point reversal. The rebound points to renewed business investment appetite heading into the new year.

The economy is sending mixed signals, which is nothing new. Cooling growth, sticky inflation, and a shifting tariff landscape were the story in 2025 and look to be carrying over into 2026. I'll keep watching the data and will keep you updated.