Three Headlines That Shouldn't Coexist

The economy added 178K jobs, the S&P posted its best week since the war began, and oil is still above $100. Three headlines that shouldn't coexist, but here we are. The catch is that most of the data we're looking at was collected before the war's economic impact had time to show up. Hiring surveys, consumer spending, and factory orders all reflect decisions made weeks or months ago. The real tell will come as companies begin reporting first quarter earnings over the next few weeks, and more importantly, what they say about the rest of the year.

Iran War & Markets

President Trump addressed the nation in a primetime speech, his first since Operation Epic Fury began on February 28. The headline: the war is "nearing completion," with a two-to-three-week window to either reach a deal with Iran or escalate to strikes on power plants and oil infrastructure. No concrete exit strategy was offered. Oil prices spiked in the sessions that followed, and Asian equities initially sold off. The message markets heard: this isn't ending soon, and the odds of things getting worse just went up.

The Strait of Hormuz has been effectively closed to most commercial shipping since early March, taking roughly 20% of global oil supply and 20% of global LNG (liquefied natural gas) off the table. Brent crude, the global benchmark for oil prices, has traded in a roughly $85–$120 range over the past month, with brief dips on ceasefire hopes and sharp spikes on escalation. At the pump, gas has crossed $4/gallon and diesel has topped $5, which flows straight into freight costs, food prices, and virtually every supply chain you can name. The under-discussed story is infrastructure damage. The International Energy Agency (IEA) has counted more than 40 Middle Eastern energy assets "severely damaged," and 17% of Qatar's LNG export capacity carries a 3–5 year repair timeline. Even if a ceasefire materializes tomorrow, supply recovery is measured in months to years, not weeks.

Goldman Sachs has raised its U.S. recession probability to 30%. The European Central Bank held rates in March, with markets now pricing in hikes rather than the cuts expected before the war. Oxford Economics pegs $140 sustained oil as the "breaking point" that tips the eurozone, UK, and Japan into recession. For the Fed, this is the worst kind of problem: inflation driven by supply shortages rather than consumer demand. Raising interest rates doesn't fix a supply problem. It just slows an already-fragile economy.

Whatever back-channel diplomacy existed appears to have collapsed. Trump had previously set April 6 as a deadline for Iran to reopen the Strait, but didn't mention it during his address. The UK hosted a summit of more than 40 countries to discuss reopening Hormuz. The U.S. did not attend. No coalition member publicly committed to using force while fighting continues. The world is waking up to the economic damage, but there's no plan yet to fix it.

Winners and losers so far: Despite the uncertainty, the S&P 500 closed the week higher, up 3.4%. The bigger story is underneath the surface. Energy stocks (XLE) have significantly outpaced the broader market year-to-date, with oil majors, refiners, and pipeline operators generating record cash flows. Defense names have similarly outperformed. On the other side, non-essential consumer spending sectors, airlines, and anything where raw material costs eat into profits remain under pressure.

Labor Market

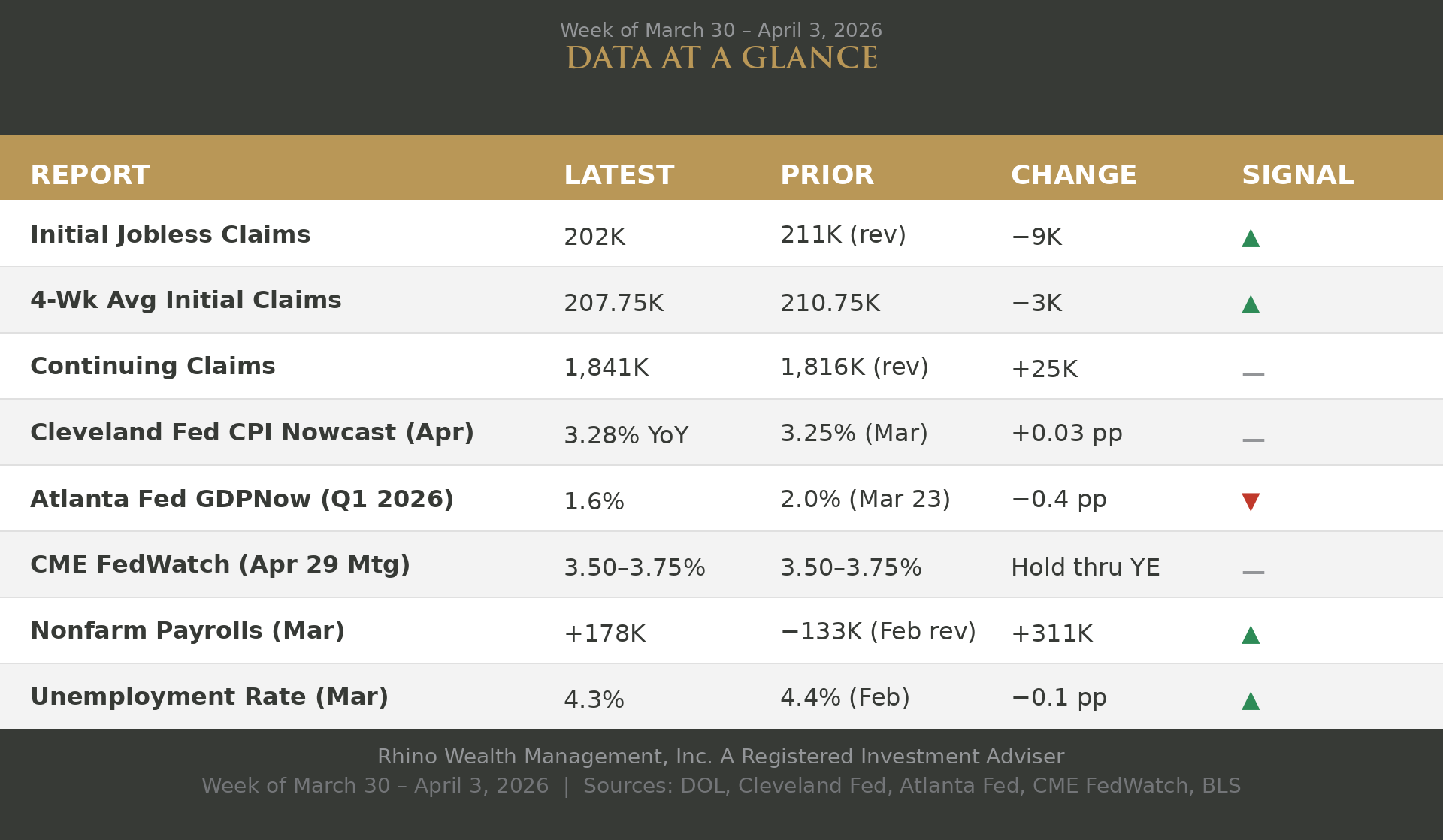

The March jobs report came in well above expectations at +178K, nearly triple the 60K consensus, with the unemployment rate ticking down to 4.3%. Healthcare led the gains, partly boosted by about 31K Kaiser Permanente nurses returning from a strike that had depressed February's numbers. The supporting data painted a fuller picture. The JOLTS report (the government's monthly measure of job openings, hires, and quits) showed hiring at its slowest pace since April 2020, while the quits rate fell to 1.9%, meaning fewer workers feel confident enough to leave their jobs. The Challenger report, a monthly tally of announced corporate layoffs, showed AI cited as the leading reason for job cuts for the first time, accounting for 25% of March layoffs. The pattern is what we've seen for months: a low-hire, low-fire labor market. Companies aren't aggressively adding headcount, but they aren't cutting it either. Weekly initial jobless claims fell to 202K, near a 2026 low. For the Fed, it's an economy that isn't hot enough to hike and isn't cold enough to cut.Consumer & Retail

Consumers are in better shape than expected. The Conference Board's Consumer Confidence Index rose to 91.8 in March, the second straight monthly gain and well above the 87.8 consensus forecast. The Present Situation Index, which measures how people feel about jobs and current income, jumped 4.6 points to 123.3. On the spending side, February retail sales rose 0.6% month-over-month, the strongest print in seven months, with broad-based gains in department stores, clothing, and health and personal care. The control group, which feeds directly into GDP calculations, came in at +0.5%, also beating expectations. The one area to watch: 12-month inflation expectations jumped in the survey, and spending plans are tilting toward essentials over big-ticket discretionary purchases. With gas prices rising sharply in March, household budgets have less room for everything else. Every extra dollar spent at the pump is a dollar that doesn't go to restaurants, retail, or travel. The next few reports will tell us whether consumers can keep this momentum going.

Housing

Home prices are still rising, but barely. The S&P Case-Shiller National Home Price Index, which runs on a two-month lag, posted a 0.9% annual gain in January, down from 1.1% in December and the weakest reading since the early 2010s. Adjust for inflation and the picture flips: with CPI running at 2.4% over the same period, home values actually lost ground in real terms over the past year. The geographic story is uneven. New York led at +4.9% and Chicago at +4.6%, while Tampa fell 2.5%, extending over a year of declines. On rates, the 30-year fixed mortgage averaged 6.46% per Freddie Mac's latest reading, up from the sub-6% levels buyers briefly saw in February. For buyers, the math hasn't changed much: prices are flat in real terms, but borrowing costs remain stubbornly high enough to keep affordability tight.

Manufacturing

Factories are expanding, but the bill is getting expensive. The ISM Manufacturing PMI, a monthly survey of purchasing managers that serves as a health check on U.S. factory activity, ticked up to 52.7 in March, a third straight month of expansion and the best run since mid-2022. Anything above 50 signals growth, so factories are clearly in gear. The problem is what it costs to keep them there. The survey's Prices Index has spiked nearly 20 points in two months to 78.3, its highest level since the supply chain chaos of 2022. Energy, chemicals, and metals are leading the increase. Employment stayed in contraction at 48.7, with survey respondents citing uncertainty around trade policy and the Middle East as reasons they're holding headcount steady and running overtime rather than adding workers. Production is up. Costs are up more.

Takeaway

There's a lot we don't know right now. How long the war lasts. What oil does next. Whether the Fed blinks. I don't have a crystal ball, and you should be cautious of anyone who speaks with certainty about what happens next. What we do know is that the labor market is intact, consumers are still spending, and the economy entered this period on solid footing. That matters. The weeks ahead will test that foundation, and we'll be watching closely.

Disclosure

This material is provided by Todd Van Der Meid, MBA, CFP®, through Rhino Wealth Management, Inc., a Registered Investment Adviser, solely for informational purposes. It is not intended as investment, tax, legal, or accounting advice. Investors should consult qualified professionals before making financial decisions.

Opinions expressed herein are general in nature and not tailored to individual circumstances. Investment strategies discussed may not be suitable for every investor. All investments carry risk, including possible loss of principal, and past performance does not guarantee future results. No investment strategy or risk management technique ensures profit or eliminates risk in all market conditions.

Investments in foreign or emerging markets involve additional risks, such as currency fluctuations, geopolitical instability, and varying accounting standards. Sector-specific investments can be more volatile due to their concentrated nature. References to indexes are for illustrative purposes; indexes are unmanaged, cannot be invested into directly, and their performance does not reflect fees, expenses, or sales charges. Index performance is not indicative of specific investment performance.

Economic forecasts and forward-looking statements reflect current views and assumptions and are subject to change. Actual results may vary materially due to market or other conditions. There is no obligation to update forward-looking information.

Information presented herein comes from reliable third-party sources but is not guaranteed for accuracy or completeness. Rhino Wealth Management, Inc. disclaims liability for errors or omissions. Portions of this content may be generated using advanced analytical tools, including artificial intelligence, and all such content has been reviewed and validated by Todd Van Der Meid, MBA, CFP®, using proprietary quality-control measures. Rhino Wealth Management, Inc. does not directly hold securities; however, securities mentioned may be included within recommended portfolio models or held by clients. Please refer to our Form ADV for additional details regarding potential conflicts of interest.