Trump's Fed Pick Shakes Markets

News That Moved Markets This Week

President Trump nominated Kevin Warsh to lead the Federal Reserve, the government agency that controls interest rates. Trump has consistently pushed for lower rates, which make it cheaper for people and businesses to borrow money. But of the candidates Trump was considering, Warsh may have been the least likely to simply do what the president wants.

Warsh, 55, previously served at the Fed from 2006 to 2011. He quit because he disagreed with the Fed’s strategy of pumping trillions of dollars into the financial system to boost the economy, a practice known as quantitative easing. His central argument is that the Fed has made it too easy for Congress to spend money it doesn’t have. In a 2025 speech, he argued that lawmakers “found it considerably easier appropriating money knowing that government’s financing costs would be subsidized by the central bank.” He wants the Fed to stop cushioning the consequences of government overspending and return to a narrow focus on keeping prices stable.

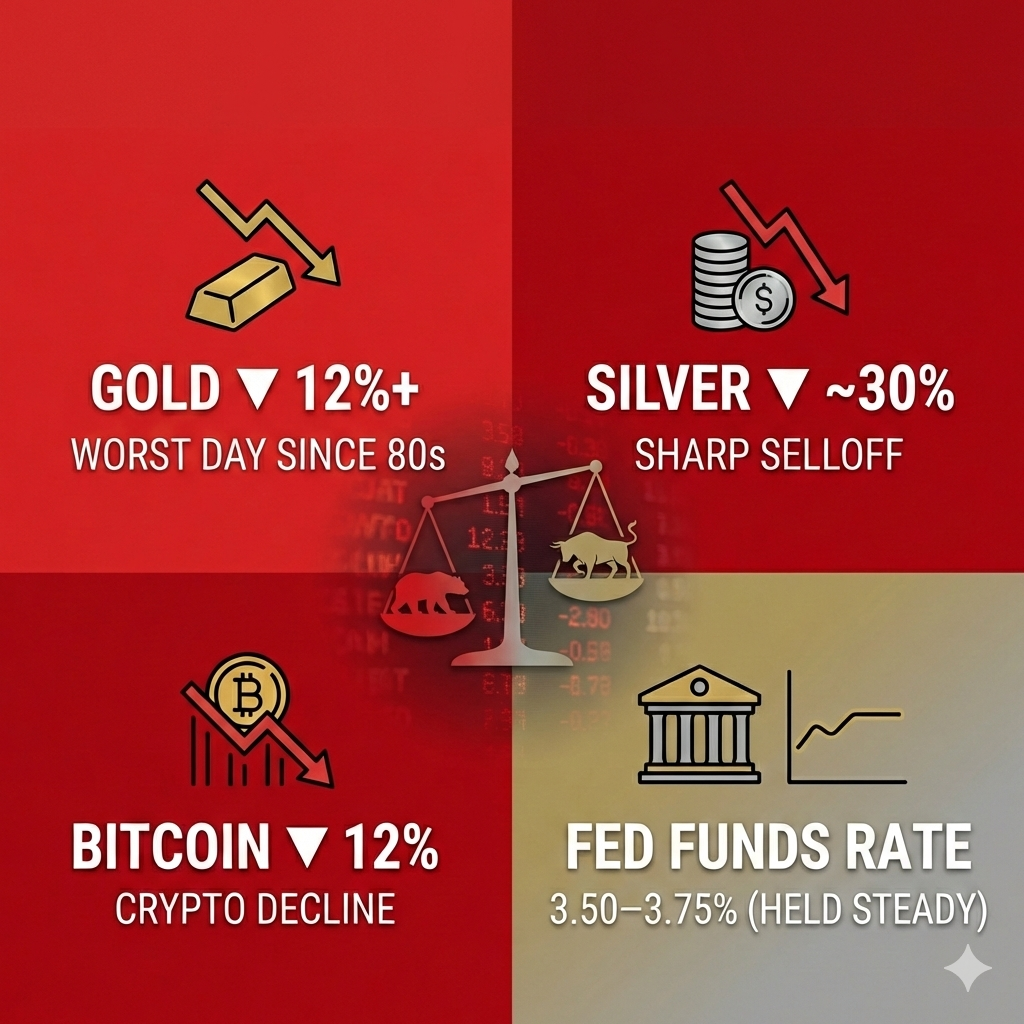

Markets reacted with force. Gold suffered its worst single-day drop since the early 1980s, falling more than 12% from record highs. Silver plunged roughly 30%. Bitcoin tumbled approximately 12%. All three assets tend to rise when investors expect easy money and a weaker dollar, conditions that make hard assets and alternatives to traditional currency more attractive. A Fed chair committed to tighter policy and a stronger dollar reverses that logic, and markets moved accordingly. Given Warsh’s public criticism of government overspending, the Senate confirmation process should be interesting.

The Fed held the federal funds rate steady at 3.5%–3.75% at its January 28 meeting, pausing after three consecutive cuts in late 2025 that were part of a broader easing cycle totaling 1.75%. The decision was widely expected. Governors Stephen Miran and Christopher Waller dissented, both favoring an additional 0.25% cut.

The committee noted solid economic expansion, low but stabilizing job gains, and somewhat elevated inflation. The statement reinforced that future rate adjustments will depend on incoming data, the evolving outlook, and the balance of risks.

Source: Federal Reserve FOMC Statement and Press Conference, January 28, 2026.

Economic Summary

The headline numbers tell a story of resilience. The Atlanta Federal Reserve Bank’s GDPNow model estimates fourth quarter 2025 growth at 4.2%, unemployment holds at 4.4%, and weekly jobless claims remain historically low at 209,000.¹ If you stopped there, you’d think the economy was humming. But the details underneath those numbers deserve a closer look.

Start with the consumer. Spending grew 0.5% in both October and November, but disposable income grew just 0.1% and 0.3% over those same months. That gap has to come from somewhere. Credit card balances hit a record $1.233 trillion in the third quarter of 2025, and the personal savings rate has fallen to 3.5%, well below its 20-year average of 5.9%.² Consumers aren’t pulling back yet, but they’re increasingly funding their spending through debt and shrinking savings rather than growing paychecks. That’s a pattern that works until it doesn’t. Meanwhile, the labor market is cooling quietly. The economy added just 49,000 jobs per month in 2025, a sharp drop from 168,000 in 2024. Employers aren’t laying people off in large numbers, but they’re not hiring either.

Inflation adds another layer of difficulty. Consumer prices are up about 2.4% from a year ago, but the broader measures the Federal Reserve watches most closely, including core Personal Consumption Expenditures (the Federal Reserve’s preferred inflation gauge), are running hotter at 2.8%.³ That’s close enough to feel progress but far enough from the 2% target to keep the Federal Reserve cautious. Futures markets are currently pricing in at most two rate cuts through the end of 2027. Borrowing costs aren’t coming down anytime soon.

Then there’s the question hanging over corporate America’s biggest bet. Hundreds of billions of dollars are flowing into artificial intelligence infrastructure, but profitability remains unproven. PJM Interconnection, the nation’s largest regional power grid operator serving 67 million people, just lowered its electricity demand forecast after finding that many planned data center projects lack firm construction or service commitments.⁴ The buildout is real, but so is the uncertainty about whether demand will match the investment.

The economy isn’t breaking. But the sources of growth are narrowing, and some of what looks like strength is being funded by debt and declining savings. For investors and planners, the takeaway is straightforward: don’t mistake headline resilience for broad-based strength, and plan accordingly for an environment where borrowing costs stay elevated and consumer momentum gradually fades.

¹ Federal Reserve Bank of Atlanta, GDPNow (January 29, 2026); Bureau of Labor Statistics, Employment Situation (January 9, 2026); Department of Labor, Weekly Claims Report (January 29, 2026).

² Federal Reserve Bank of New York, Household Debt and Credit Report (Q3 2025); Bureau of Economic Analysis, Personal Income and Outlays (January 22, 2026).

³ Federal Reserve Bank of Cleveland, Inflation Nowcasting (January 30, 2026); CME Group FedWatch Tool (January 31, 2026).

⁴ PJM Interconnection, Load Forecast Report (January 14, 2026).

Disclosure

This material is provided by Todd Van Der Meid, MBA, CFP®, through Rhino Wealth Management, Inc., a Registered Investment Adviser, solely for informational purposes. It is not intended as investment, tax, legal, or accounting advice. Investors should consult qualified professionals before making financial decisions.

Opinions expressed herein are general in nature and not tailored to individual circumstances. Investment strategies discussed may not be suitable for every investor. All investments carry risk, including possible loss of principal, and past performance does not guarantee future results. No investment strategy or risk management technique ensures profit or eliminates risk in all market conditions.

Investments in foreign or emerging markets involve additional risks, such as currency fluctuations, geopolitical instability, and varying accounting standards. Sector-specific investments can be more volatile due to their concentrated nature. References to indexes are for illustrative purposes; indexes are unmanaged, cannot be invested into directly, and their performance does not reflect fees, expenses, or sales charges. Index performance is not indicative of specific investment performance.

Economic forecasts and forward-looking statements reflect current views and assumptions and are subject to change. Actual results may vary materially due to market or other conditions. There is no obligation to update forward-looking information.

Information presented herein comes from reliable third-party sources but is not guaranteed for accuracy or completeness. Rhino Wealth Management, Inc. disclaims liability for errors or omissions. Portions of this content may be generated using advanced analytical tools, including artificial intelligence, and all such content has been reviewed and validated by Todd Van Der Meid, MBA, CFP®, using proprietary quality-control measures. Rhino Wealth Management, Inc. does not directly hold securities; however, securities mentioned may be included within recommended portfolio models or held by clients. Please refer to our Form ADV for additional details regarding potential conflicts of interest.