Why Mortgage Rates Went Up When the Fed Cut Rates

This week, the Federal Reserve's Federal Open Market Committee (FOMC) voted to lower the Fed Funds rate by 0.25%. While rate cuts are generally intended to reduce borrowing costs and support economic growth, the bond market's response reflected a more complex picture—yields on longer-term bonds moved higher. This divergence suggests that investors are weighing factors beyond the Fed's near-term policy, including inflation risks, economic resilience, and the outlook for future rate decisions.

Why Did Long-Term Yields Rise?

1. Mixed Signals from the Fed

Although the Fed lowered rates, Chair Jerome Powell emphasized caution about future cuts. His remarks introduced uncertainty into the market, leading investors to conclude that additional rate reductions may not be forthcoming. Powell stated, "A further reduction in the policy rate at the December meeting is not a foregone conclusion. Far from it." This statement highlighted internal divisions within the Federal Open Market Committee and signaled that future rate cuts are far from guaranteed.

2. Economic Data

Recent reports show that consumer spending remains solid. However, while official government data is unavailable due to the shutdown, private-sector sources suggest that hiring has slowed, and job growth may be weakening. In the absence of fresh data from the Bureau of Labor Statistics, investors are relying on alternative indicators, which point to a softening but not collapsing, labor market.

3. Inflation Expectations

Investors are watching inflation closely. If they expect it to remain elevated or rise again, they demand higher yields on long-term bonds to protect their purchasing power. This is because inflation erodes the real value of future interest payments. To compensate for that risk, investors require a higher return—known as the inflation risk premium. Additionally, strong economic data and wage growth can reinforce expectations of persistent inflation, further pushing yields higher.

4. Government Debt Issuance

The federal government continues to borrow heavily to fund spending. If fewer investors are willing to buy that debt, bond prices fall and yields rise to attract buyers.

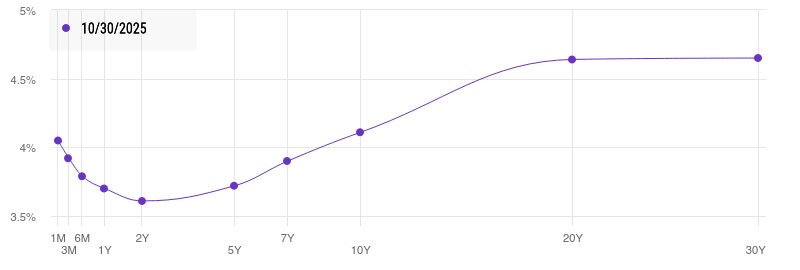

5. Reconciling the Yield Curve with Late-Cycle Signals

The yield curve—which compares short- and long-term interest rates—is beginning to steepen. This shift often suggests investors are moving away from recession concerns and toward expectations of continued growth and inflation. Historically, a steepening curve can occur in two distinct phases of the business cycle:

- Early-cycle recovery, when markets anticipate economic acceleration after a downturn.

- Late-cycle transition, when inflation expectations rise and long-term rates increase due to fiscal deficits, supply constraints, or persistent wage pressures.

Currently, many economic indicators point to a late-cycle environment:

- Labor market softening: Unemployment has edged up to 4.3% from cycle lows, and job creation is slowing.

- Treasury Yield Curve Chart

6. Mortgage Rates and the 10-Year Treasury

Mortgage rates also rose following the Fed's announcement, underscoring an important distinction in how different interest rates respond to monetary policy. While the Fed directly controls short-term rates like the Fed Funds rate, mortgage rates are more closely tied to the 10-year Treasury yield. As long-term bond yields climbed in response to the factors outlined above, mortgage rates followed suit. Mortgage bond buyers are more sensitive to the bond market's assessment of long-term economic conditions than to the Fed's immediate policy moves.